How Many Discount Points Can You Buy on a Mortgage?

January 6, 2026How Many Discount Points Can You Buy?

The short answer: Most lenders allow 3-4 discount points maximum, though some may allow more. But should you buy that many? Let's break it down.

Typical Limits by Lender

| Lender Type | Typical Maximum Points |

|---|---|

| Conventional | 3-4 points |

| FHA | 2-3 points |

| VA | 2 points (seller limits) |

| Jumbo | 4+ points |

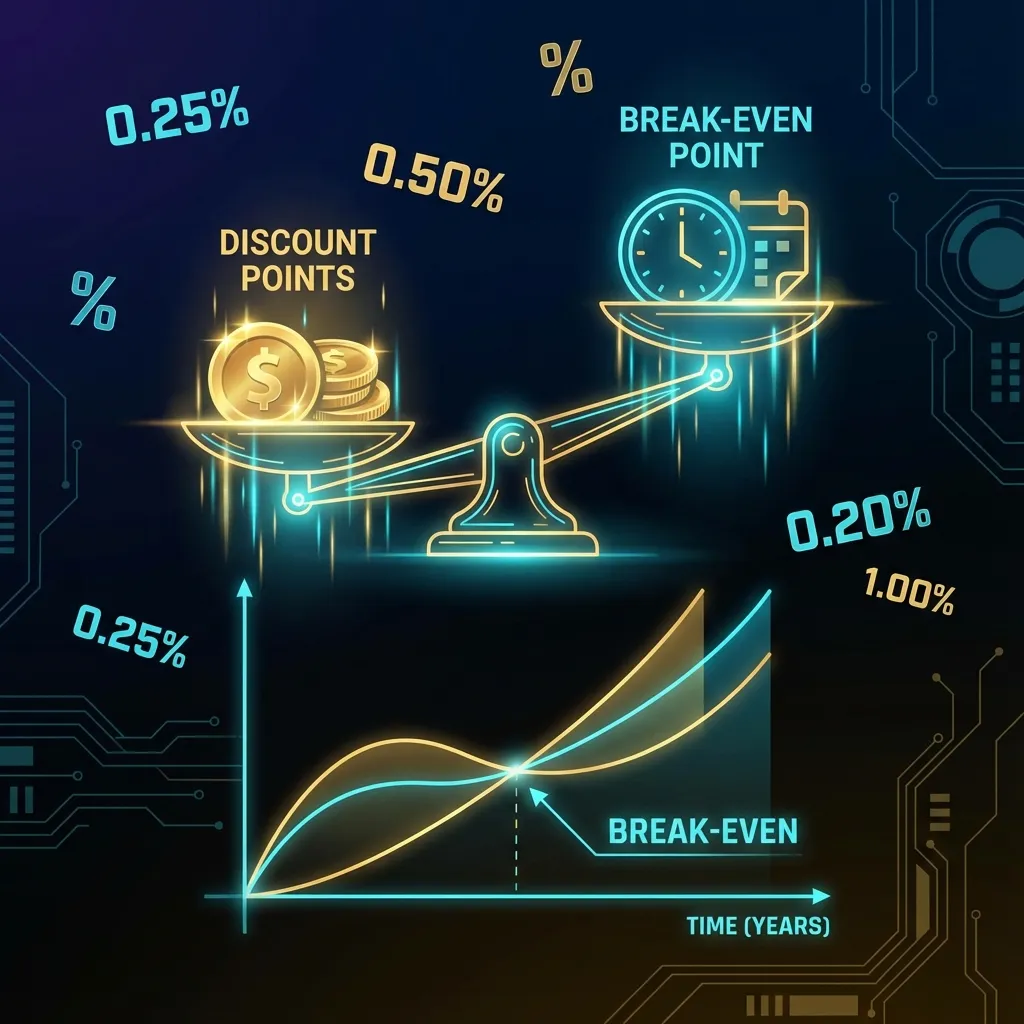

The Law of Diminishing Returns

Here's the key insight most borrowers miss: the more points you buy, the less value each additional point provides.

| Points | Rate Reduction | Break-Even |

|---|---|---|

| 1 point | 0.25% | ~5 years |

| 2 points | 0.50% | ~5.5 years |

| 3 points | 0.75% | ~6 years |

| 4 points | 1.00% | ~6.5 years |

When Buying Multiple Points Makes Sense

✅ Buy more points if:

- You're certain you'll keep the loan 10+ years

- You have excess cash at closing

- You're in the highest tax bracket (potential deduction)

- Rates are historically high and won't drop soon

❌ Buy fewer (or no) points if:

- You might refinance in 3-5 years

- You need that cash for other purposes

- Rates are expected to drop significantly

Calculate Your Optimal Points

Use our Discount Points Break-Even Calculator to find the sweet spot for your situation.

LO Script: Explaining Points Limits to Clients

"Most lenders cap points at 3-4, but honestly, buying more than 2 points rarely makes sense. Here's why: each additional point takes longer to pay off. Let me show you the math for your specific loan..."

Need to create a points comparison for your client? Use ShowTheRate to build a professional analysis in 60 seconds.

💡 Ready to put this knowledge into action?

Try Our Free Calculators